DEF 14A: Definitive proxy statements

Published on August 13, 2021

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement

Pursuant to Section 14(a) of the Securities

Exchange Act of

1934

(Amendment No. )

|

Filed by the Registrant |  |

Filed by a Party other than the Registrant |

| Check the appropriate box: | |

|

Preliminary Proxy Statement |

|

CONFIDENTIAL, FOR USE OF THE COMMISSION ONLY (AS PERMITTED BY RULE 14a-6(e)(2)) |

|

Definitive Proxy Statement |

|

Definitive Additional Materials |

|

Soliciting Material under to §240.14a-12 |

Korn Ferry

![]()

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

| Payment of Filing Fee (Check the appropriate box): | |

|

No fee required. |

|

Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) Title of each class of securities to which transaction applies: | |

| (2) Aggregate number of securities to which transaction applies: | |

| (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): | |

| (4) Proposed maximum aggregate value of transaction: | |

| (5) Total fee paid: | |

|

Fee paid previously with preliminary materials. |

|

Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| (1) Amount Previously Paid: | |

| (2) Form, Schedule or Registration Statement No.: | |

| (3) Filing Party: | |

| (4) Date Filed: | |

![]()

Dear Fellow Stockholders,

On behalf of the Board of Directors (the “Board”) of Korn Ferry (the “Company,” “we,” “its,” and “our”) and all of our Korn Ferry colleagues, I want to thank you for being a Korn Ferry stockholder and for your continued support of the Company. In May 2020, as the Company entered its fiscal year 2021, the world faced considerable uncertainty with the broad challenges of the coronavirus pandemic (“COVID-19”) and its attendant social and economic instability across the globe. Our Board and management team worked tirelessly to navigate the Company through the pandemic and remained fiercely committed to devising ways to preserve and deliver value to our stockholders, while simultaneously pursuing Korn Ferry’s long-term strategy.

Thanks to the agility and resilience of Korn Ferry’s employees and their effective execution of our strategy, Korn Ferry emerged through the crisis with a record breaking fourth quarter. As our 2021 Annual Meeting of Stockholders approaches, we are pleased to share our reflections on how we worked to deliver strong results for Korn Ferry’s stockholders during such an unprecedented year.

As the pandemic has persisted, we have remained focused and dedicated to pursuing Korn Ferry’s objective to expand its position as the preeminent organizational consulting firm. With the support of our workforce during fiscal year 2021, we continued to diversify our offerings, develop deeper relationships with our clients, and capitalize on our leadership in various solutions. The relevance of our wide array of offerings have helped our clients address their opportunities and achieve their goals. In turn, it has helped us accelerate out of the turn and deliver strong financial results.

From a tough first quarter in fiscal year 2021, Korn Ferry achieved all-time highs for quarterly fee revenues and profitability by the fourth quarter. We are proud of our people and their leaders, who so productively managed to continue to serve our clients despite shifting work locations, technological and personal demands, and related lockdowns and limitations. Their achievements are all the more significant due to the speed with which these disruptions arose and the demand for a rapid response. With their help, we were able to quickly and effectively adapt to delivering our services in a virtual world.

On behalf of the Board, I am pleased to invite you to attend our 2021 Annual Meeting of Stockholders on Wednesday, September 29, 2021 at 8:00 a.m. Pacific Time. In light of the continued public health impact of COVID-19, the meeting will be conducted online this year through a live audiocast, which is often referred to as a “virtual meeting” of stockholders. Our digital format allows stockholders to participate safely, conveniently, and effectively. We intend to hold our virtual meeting in a manner that affords stockholders the same general rights and opportunities to participate, to the extent possible, as they would have at an in-person meeting. We look forward to your participation at the 2021 Annual Meeting of Stockholders.

Sincerely,

Christina A. Gold,

Chair of the Board

August 13, 2021

Korn Ferry

1900 Avenue of the Stars, Suite 2600

Los Angeles, CA 90067

(310) 552-1834

|

i

|

Notice of

2021 Annual Meeting

Meeting Information

Date: September 29, 2021

Time: 8:00 a.m. Pacific Time

Virtual Meeting Site: www.virtualshareholdermeeting.com/KFY2021

Record Date: August 2, 2021

Meeting Agenda

To the Stockholders:

In light of the public health and travel safety concerns relating to the coronavirus pandemic (“COVID-19”), on September 29, 2021, Korn Ferry (the “Company,” “we,” “its,” and “our”) will hold its 2021 Annual Meeting of Stockholders (the “Annual Meeting”) online this year at www.virtualshareholdermeeting.com/KFY2021. The Annual Meeting will begin at 8:00 a.m. Pacific Time.

The purposes of the Annual Meeting are to:

| 1. | Elect the nine directors nominated by our Board of Directors (the “Board”) and named in the Proxy Statement accompanying this notice to serve on the Board until the 2022 Annual Meeting of Stockholders and until their successors have been duly elected and qualified, subject to their earlier death, resignation, or removal; |

| 2. | Vote on a non-binding advisory resolution to approve the Company’s executive compensation; |

| 3. | Ratify the appointment of Ernst & Young LLP as the Company’s independent registered public accounting firm for the Company’s 2022 fiscal year; and |

| 4. | Transact any other business that may be properly presented at the Annual Meeting. |

Only stockholders who owned our common stock as of the close of business on August 2, 2021 (the “Record Date”) can vote online at the Annual Meeting or any adjournments or postponements thereof. To attend the Annual Meeting online, vote or submit questions during the Annual Meeting, or view the stockholder list, stockholders of record will need to go to www.virtualshareholdermeeting.com/KFY2021 and log in using their 16-digit control number included on their proxy card or Notice of Internet Availability of Proxy Materials (the “Notice’). Beneficial owners should review these proxy materials and their voting instruction form or the Notice for how to vote in advance of, and how to participate in, the Annual Meeting.

RECOMMENDATION

OF THE BOARD

THE BOARD UNANIMOUSLY RECOMMENDS THAT YOU VOTE YOUR SHARES “FOR” THE ELECTION OF EACH OF THE NOMINEES NAMED IN THE PROXY STATEMENT AND “FOR” EACH OF THE OTHER PROPOSALS.

In the event of a technical malfunction or situation that the chair of the Annual Meeting determines may affect the ability of the Annual Meeting to satisfy the requirements for a meeting of stockholders to be held by means of remote communication under the Delaware General Corporation Law, or that otherwise makes it advisable to adjourn the Annual Meeting, the chair of the Annual Meeting will convene the meeting at 9:00 a.m. Pacific Time on the date specified above and at the Company’s address at 1900 Avenue of the Stars, Suite 2600, Los Angeles, CA 90067, solely for the purpose of adjourning the Annual Meeting to reconvene at a date, time, and physical or virtual location announced by the chair of the Annual Meeting. Under either of the foregoing circumstances, we will post information regarding the announcement on the Investors page of the Company’s website at https://ir.kornferry.com.

Please read the proxy materials carefully before voting.

Your vote is important, and we appreciate your cooperation in considering and acting on the matters presented. See pages 75 – 77 in the accompanying Proxy Statement for a description of the ways by which you may cast your vote on the matters being considered at the Annual Meeting.

August 13, 2021

Los Angeles, California

By Order of the Board of Directors,

Jonathan Kuai

General Counsel, Managing Director of Business Affairs and

ESG, and Corporate Secretary

Important Notice Regarding the Availability of Proxy Materials for the Stockholder Meeting to be Held on September 29, 2021:

The Proxy Statement and accompanying Annual

Report to Stockholders are available at

www.proxyvote.com.

Proxy Summary

This summary highlights information contained elsewhere in this Proxy Statement. This summary does not contain all of the information that you should consider, and you should read the entire Proxy Statement carefully before voting. Page references are supplied to help you find further information in this Proxy Statement.

Annual Meeting of Stockholders (page 75)

Date and Time: September 29, 2021 at 8:00 a.m. Pacific Time

Virtual Meeting Site: www.virtualshareholdermeeting.com/KFY2021

Admission: To participate in the Annual Meeting online, including to vote during the Annual Meeting, stockholders will need the 16-digit control number included on their proxy card, the Notice or voting instruction form, or contact their bank, broker or other nominee (preferably at least 5 days before the Annual Meeting) and obtain a “legal proxy” in order to be able to attend, participate in, or vote at the Annual Meeting.

Eligibility to Vote: You can vote if you were a holder of Korn Ferry’s common stock at the close of business on August 2, 2021.

| Voting Matters (page 75) | |

| 1 |

Election of Directors Reference (for more detail) page 12 |

Board

Vote Recommendation FOR each Director Nominee |

| 2 |

Advisory Resolution to Approve Executive Compensation Reference (for more detail) page 33 |

Board

Vote Recommendation FOR |

| 3 |

Ratification of Independent Registered Public Accounting Firm Reference (for more detail) page 68 |

Board

Vote Recommendation FOR |

How to Cast Your Vote (pages 75 - 77)

On or about August 13, 2021, we will mail the Notice to stockholders of our common stock as of August 2, 2021, other than those stockholders who previously requested electronic or paper delivery of communications from us. Stockholders can vote by any of the following methods:

|

Via telephone by calling 1-800-690-6903; |

|

Via Internet: Before the Annual Meeting by visiting www.proxyvote.com; During the Annual Meeting by visiting www.virtualshareholdermeeting.com/KFY2021; or |

|

Via mail (if you received your proxy materials by mail) by signing, dating, and mailing the enclosed proxy card. |

| • | If you vote via telephone, you must vote no later than 11:59 p.m. Eastern Time on September 28, 2021. If you return a proxy card by mail, it must be received before the polls close at the Annual Meeting. |

|

1

|

Highlights for Fiscal Year 2021

Business Performance

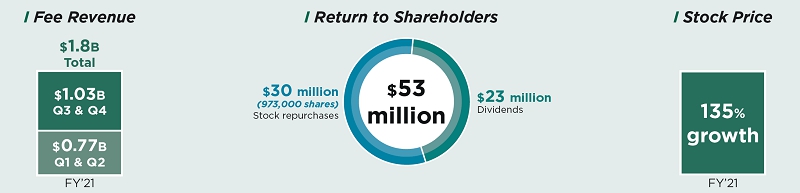

| I | Generated all-time high quarters of Net Income Attributable to Korn Ferry of $51.3 million and $66.2 million with Operating Margins of 13.7% and 15.5%, and Adjusted Net Income Attributable to Korn Ferry* of $51.9 million and $66.2 million, in the third and fourth quarters of fiscal year 2021, respectively. This compares to $20.0 million and $(0.8) million of Net Income (Loss) Attributable to Korn Ferry with Operating Margins of 6.1% and 5.0%, and $41.0 million and $32.7 million of Adjusted Net Income Attributable to Korn Ferry* in the third and fourth quarters in the fiscal year 2020, respectively. |

| I | Achieved all-time high quarters of Adjusted EBITDA* of $96.7 million and $112.8 million, and a 20.3% Adjusted EBITDA margin*, in the third and fourth quarters of fiscal year 2021. |

| I | Achieved all-time high in both Diluted Earnings Per Share of $0.94 and $1.21, and Adjusted Diluted Earnings Per Share* of $0.95 and $1.21, in the third and fourth quarters of fiscal year 2021, respectively. |

| * | Adjusted Net Income Attributable to Korn Ferry, Adjusted Diluted Earnings Per Share, Adjusted EBITDA, and Adjusted EBITDA margin are non-GAAP financial measures. For a discussion of these measures and for reconciliation to the nearest comparable GAAP measures, see Appendix A to this Proxy Statement. |

|

2

|

| COVID-19 Response | |

|

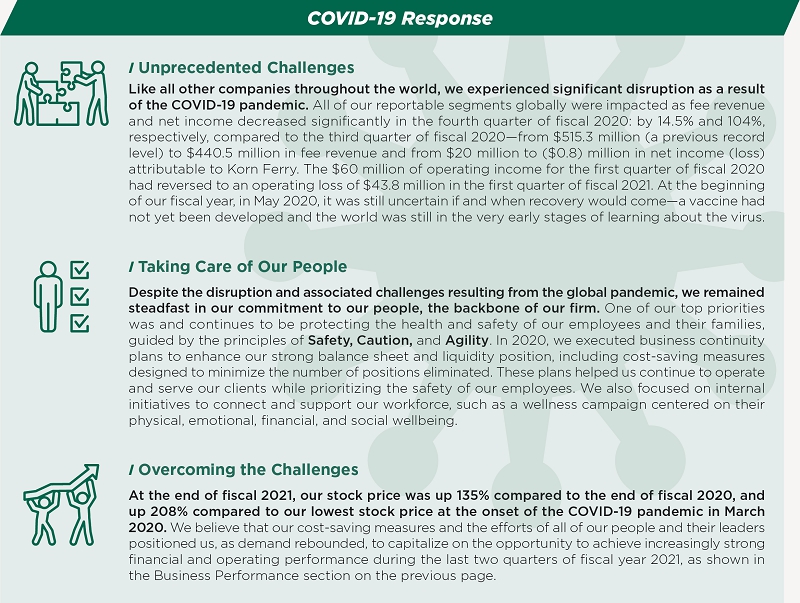

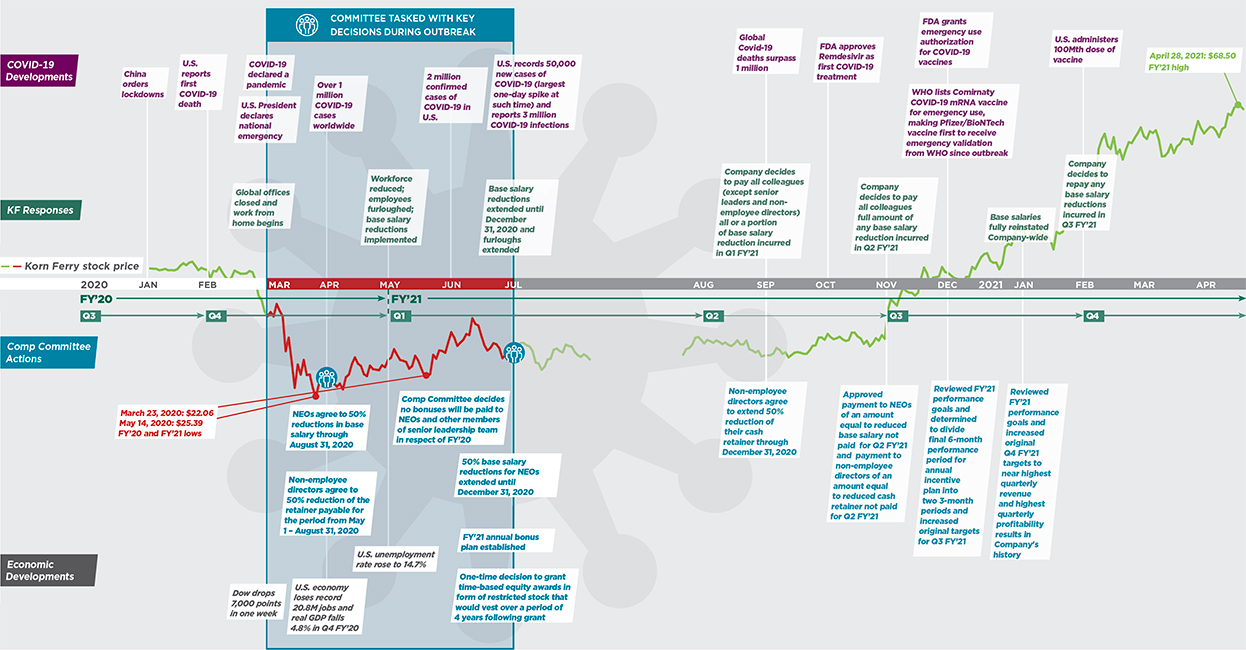

I Unprecedented Challenges Like all other companies throughout the world, we experienced significant disruption as a result of the COVID-19 pandemic. All of our reportable segments globally were impacted as fee revenue and net income decreased significantly in the fourth quarter of fiscal 2020: by 14.5% and 104%, respectively, compared to the third quarter of fiscal 2020—from $515.3 million (a previous record level) to $440.5 million in fee revenue and from $20 million to ($0.8) million in net income (loss) attributable to Korn Ferry. The $60 million of operating income for the first quarter of fiscal 2020 had reversed to an operating loss of $43.8 million in the first quarter of fiscal 2021. At the beginning of our fiscal year, in May 2020, it was still uncertain if and when recovery would come—a vaccine had not yet been developed and the world was still in the very early stages of learning about the virus. |

|

|

I Taking Care of Our People Despite the disruption and associated challenges resulting from the global pandemic, we remained steadfast in our commitment to our people, the backbone of our firm. One of our top priorities was and continues to be protecting the health and safety of our employees and their families, guided by the principles of Safety, Caution, and Agility. In 2020, we executed business continuity plans to enhance our strong balance sheet and liquidity position, including cost-saving measures designed to minimize the number of positions eliminated. These plans helped us continue to operate and serve our clients while prioritizing the safety of our employees. We also focused on internal initiatives to connect and support our workforce, such as a wellness campaign centered on their physical, emotional, financial, and social wellbeing. |

|

|

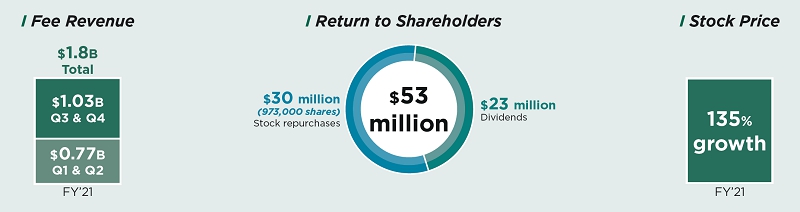

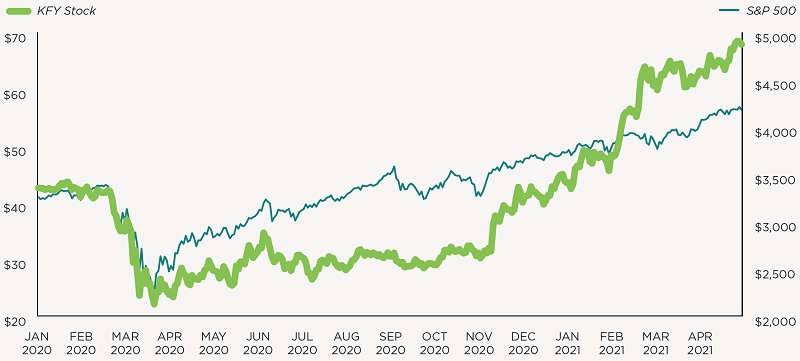

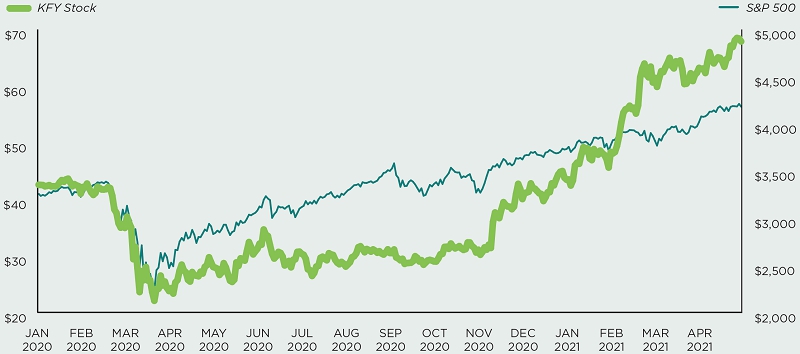

I Overcoming the Challenges At the end of fiscal 2021, our stock price was up 135% compared to the end of fiscal 2020, and up 208% compared to our lowest stock price at the onset of the COVID-19 pandemic in March 2020. We believe that our cost-saving measures and the efforts of all of our people and their leaders positioned us, as demand rebounded, to capitalize on the opportunity to achieve increasingly strong financial and operating performance during the last two quarters of fiscal year 2021, as shown in the Business Performance section on the previous page. |

Environmental, Social, and Governance (“ESG”) Accomplishments

| I | Published 2020 Corporate Responsibility Report and inaugural SASB Report. |

| I | Awarded the 2021 Silver Status Medal from EcoVadis for Corporate Social Responsibility Practices for the third consecutive year, and placed in the top 16% of the more than 75,000 companies assessed by EcoVadis based on our score. |

| I | Achieved Management Level rating for 2020 submission to the CDP Climate Change survey, which detailed our calendar year 2019 greenhouse gas emissions and climate-related practices. |

| I | Recognized by Working Mother as one of the 2020 100 Best Companies for parents to work for the second consecutive year, as one of the 2020 Best Companies for Dads, and as one of the 2020+ Top 75 Companies for Executive Women. |

| I | For the third consecutive year, earned a perfect score of 100 on the 2021 Human Rights Campaign Foundation’s Corporate Equality Index and named a “best place to work” for LGBTQ equality. |

| I | Established an independent, not-for-profit—Korn Ferry Charitable Foundation—with the mission of making real, lasting changes by helping people exceed their potential through opportunity. |

| I | Continued to achieve certification to internationally recognized standards for mature global privacy and security programs (ISO/IEC 27001:2013 and ISO/IEC 27018:2019). |

|

3

|

Corporate Governance (page 23)

| Strong Governance Practices | ||||

| Annual Director Elections for All Directors. | ||||

| Majority Voting in Uncontested Elections. | ||||

| Committee Oversight of ESG Program. | ||||

| No Supermajority Voting Standards. | ||||

| Stockholder Right (at 25% Threshold) to Call Special Stockholder Meetings. | ||||

|

|

|

||

| Board Structure | Committees, Attendance, and | Stockholder Engagement | ||

| Commitments | ||||

| Independent Chair of the Board. | Independent Audit, Compensation and Nominating Committees. | Stockholder Communication Process for Communicating with the Board. | ||

| 7 of the 8 Directors on the Board are Independent. | All Directors Attended at Least 75% of Board and Their Respective Committee Meetings. | Regular Stockholder Engagement Throughout the Year. | ||

| Independent Directors Meet in Regular Executive Sessions. | No Director Serves on More Than Four Public Company Boards. | |||

| 10-Term Service Limit for Non-Executive Directors Joining the Board after October 1, 2020. | Female Chair of the Board and 2 Committees Led by Diverse Directors (by Gender or Race/Ethnicity). | |||

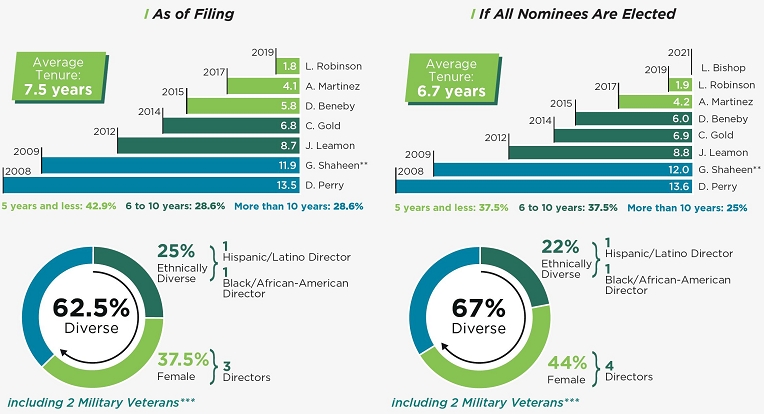

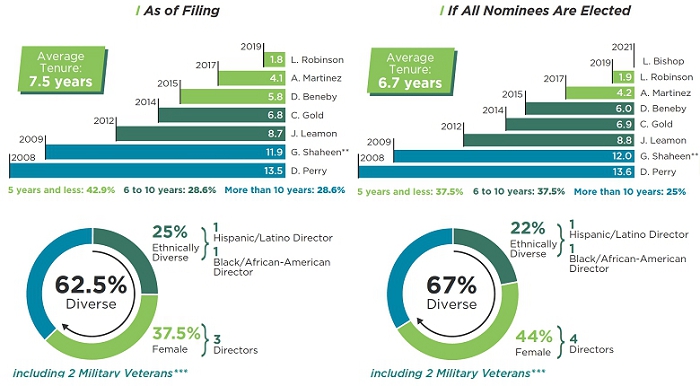

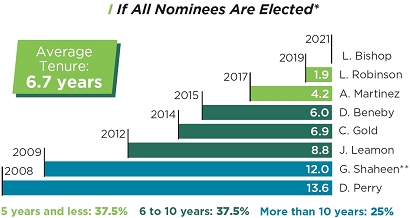

Board Tenure* and Diversity

| * | Tenure is provided for non-executive directors only. |

| ** | These graphics include Mr. Shaheen’s cumulative service with the Board from 2009 to 2019, and from April 2020 to present. |

| *** | Not included in diversity percentages. |

|

4

|

Governance Insights (pages 13, 43, and 70)

Each of the Company’s standing Board committees is committed to staying abreast of the latest issues impacting good corporate governance. The Company has included three sets of Questions & Answers (“Q&As”), one with the chair of each of the Company’s standing committees.

These Q&As are meant to provide stockholders with insight into committee-level priorities and perspectives on ESG matters, the impact of COVID-19 on compensation, and the oversight and managing COVID-19 risks.

Board Nominees (pages 17 – 22)

|

|

|

||

| Doyle N. BENEBY | Laura M. BISHOP | Gary D. BURNISON | ||

| Director | Nominee | Director and President/CEO of Korn Ferry |

||

|

Age: 61 Director Since: 2015 Independent: Yes Committee Memberships: • Nominating and Corporate Governance (Chair) • Compensation and Personnel Experience/Qualifications: • President and CEO of Midland Cogeneration Venture. • Former CEO of New Generation Power International. • Former President and CEO of CPS Energy. • Brings extensive executive management experience in the energy industry. |

Age: 59 Independent: Yes Committee Memberships: - Experience/Qualifications: • Former Executive Vice President and Chief Financial Officer of USAA. • Brings executive management, finance and investment strategy, and corporate governance experience. |

Age: 60 Director Since: 2007 Independent: No Committee Memberships: - Experience/Qualifications: • President and CEO of the Company. • Brings in-depth knowledge of the Company’s business, operations, employees, and strategic opportunities. |

|

5

|

|

|

|

||

| Christina A. GOLD | Jerry P. LEAMON | Angel R. MARTINEZ | ||

|

Director and Non-Executive Chair of the Board of Korn Ferry |

Director | Director | ||

|

Age: 73 Director Since: 2014 Independent: Yes Committee Memberships: - Experience/Qualifications: • Former President, CEO, and Director of The Western Union Company. • Brings board experience, executive management, and broad international experience. |

Age: 70 Director Since: 2012 Independent: Yes Committee Memberships: • Compensation and Personnel (Chair) • Audit Experience/Qualifications: • Former Global Managing Director of Deloitte. • Brings financial accounting expertise and extensive global professional services experience. |

Age: 66 Director Since: 2017 Independent: Yes Committee Memberships: • Audit Experience/Qualifications: • Former Chairman of the Board of Directors, and Former President and CEO, of Deckers Brands (formerly known as Deckers Outdoor Corporation). • Brings executive management, product, and marketing experience. |

||

|

|

|

||

| Debra J. PERRY | Lori J. ROBINSON | George T. SHAHEEN | ||

| Director | Director | Director | ||

|

Age: 70 Director Since: 2008 Independent: Yes Committee Memberships: • Audit (Chair) • Nominating and Corporate Governance Experience/Qualifications: • Former senior managing director in the Global Ratings and Research Unit of Moody’s Investors Service, Inc. • Brings executive management, corporate governance, finance and analytical expertise, and board and committee experience. |

Age: 62 Director Since: 2019 Independent: Yes Committee Memberships: • Compensation and Personnel • Nominating and Corporate Governance Experience/Qualifications: • Former Commander, U.S. Northern Command and NORAD (North American Aerospace Defense Command), Department of the Air Force (Ret.). • Brings significant leadership, strategy oversight and execution, and international experience and expertise. |

Age: 77 Director Since: 2020 (previously a Director from 2009-2019) Independent: Yes Committee Memberships: • Compensation and Personnel • Nominating and Corporate Governance Experience/Qualifications: • Former Non-Executive Chair of the Board of Korn Ferry and former Chief Executive Officer of Siebel Systems, Inc. • Brings executive management, consulting, board and advisory experience. |

|

6

|

2021 Executive Compensation Summary (pages 53 – 54)

|

Name and Principal Position |

Salary ($) |

Stock Awards ($) |

Non-Equity Incentive Plan Compensation ($) |

Change in Pension Value and Nonqualified Deferred Compensation Earnings ($) |

All Other Compensation ($) |

Total ($) |

||||||

|

Gary D. Burnison, President and Chief Executive Officer |

796,250 | 5,700,025 | 4,815,720 | 15,862 | 19,670 | 11,347,527 | ||||||

|

Robert P. Rozek, Executive Vice President, Chief Financial Officer and Chief Corporate Officer |

503,125 | 2,300,063 | 2,535,750 | — | 18,347 | 5,357,285 | ||||||

|

Byrne Mulrooney, Chief Executive Officer of RPO, Professional Search and Digital |

393,750 | 2,500,045 | 3,087,000 | — | 235,688 | 6,216,483 | ||||||

|

Mark Arian, Chief Executive Officer of Consulting |

393,750 | 1,600,128 | 2,646,000 | — | 262,633 | 4,902,511 |

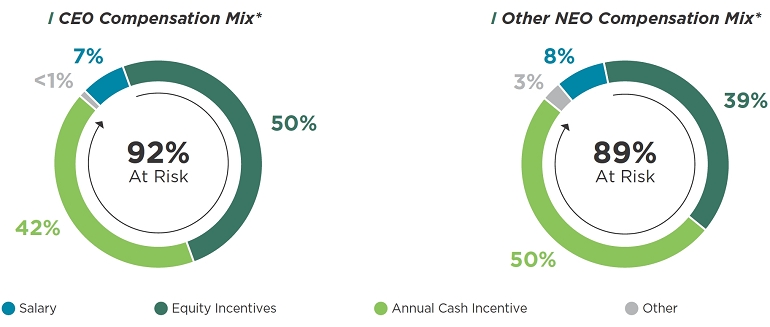

2021 Executive Total Compensation Mix (page 39)

![]()

| * | Equity awards based upon grant date value. |

|

7

|

Compensation Process Highlights (pages 27 and 39 – 42)

| • | Our Compensation and Personnel Committee receives advice from its independent compensation consultant. |

| • | We review total direct compensation and the mix of the compensation components for our named executive officers relative to our peer group as one of the factors in determining if compensation is adequate to attract and retain executive officers with the unique set of skills necessary to manage and motivate our global people and organizational consulting firm. |

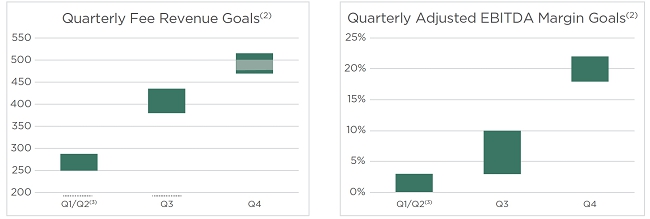

| • | As described in last year’s proxy statement, our named executive officers and non-employee directors agreed to substantial reductions (50%) in base salary and cash retainer fees, respectively, and the Compensation and Personnel Committee decided to eliminate any payouts from the Company’s short-term incentive bonus plan for fiscal year 2020 for our named executive officers as cash flow and cost-saving measures in the face of economic uncertainty created by the global COVID-19 pandemic. In designing the Company’s short-term incentive bonus plan for our named executive officers for fiscal year 2021, the Compensation and Personnel Committee initially decided to measure performance over two six-month periods and one overall one-year period (with reductions for any amounts earned during the separate six-month periods), and subsequently determined to divide the second six-month performance period into two three-month performance periods and eliminate the overall one-year performance period to allow the Compensation and Personnel Committee to take into consideration the continually evolving impact of and uneven recovery from the COVID-19 pandemic over the course of the fiscal year, resulting in setting significantly higher performance targets for the third and fourth quarters. |

As evidenced by our stock price, our Company was severely affected by the impacts of the COVID-19 pandemic and the social and political environment in the months when the Compensation and Personnel Committee was tasked with making compensation decisions. In June 2020, for the first time since our fiscal year 2009 during the Great Recession, we suspended providing financial guidance. Due to the uncertainty, the Compensation and Personnel Committee set up an annual bonus plan that allowed us to monitor the evolving economic conditions and make adjustments as needed, resulting in significantly increased performance targets for the third and fourth quarters. Additionally, as described in more detail on page 48, given that we were unable to project performance over the course of the year, the Compensation and Personnel Committee felt it was not responsible to grant long-term performance-based equity awards that would require making projections over a longer period and thus made a one-time decision to provide long-term compensation solely in the form of time-based equity awards. Nevertheless, as a result of our teams’ extraordinary efforts during these challenging times, our performance improved, with our fiscal 2021 year-end stock price up 135% compared to the end of fiscal 2020, and up 208% compared to our lowest stock price at the onset of the COVID-19 pandemic in March 2020. Beginning with fiscal year 2022, the Compensation and Personnel Committee returned to its usual practice of granting performance-based equity awards.

|

8

|

Elements of Compensation (pages 45 – 50)

| Element | Purpose | Determination | ||

| Base Salary | Compensate for services rendered during the fiscal year and provide sufficient fixed cash income for retention and recruiting purposes. | Reviewed on an annual basis by the Compensation and Personnel Committee taking into account competitive data from our peer group, input from our compensation consultant, and the executive’s individual performance. | ||

| Annual Cash Incentives | Motivate and reward named executive officers for achieving performance goals over a one-year period. | Determined by the Compensation and Personnel Committee based upon performance goals. As noted above, for fiscal year 2021, there were three separate measurement periods. Each measurement period required positive cash flow in order for any awards to be earned with respect to such period. No awards were paid until after the completion of the entire fiscal year. | ||

| Long-Term Incentives | Align the named executive officers’ interests with those of stockholders and motivate and retain top talent. | Determined by the Compensation and Personnel Committee based upon a number of factors including competitive data, total overall compensation provided to each named executive officer, and historical grants. |

Compensation Practices (page 39)

|

Our Board has adopted a clawback policy applicable to all cash incentive payments and performance-based equity awards granted to executive officers. |

|

Our named executive officers are not entitled to any “single trigger” equity acceleration in connection with a change in control. |

|

We have adopted policies prohibiting hedging, speculative trading, or pledging of Company stock. |

|

All named executive officers are subject to stock ownership requirements. |

|

We do not provide excise tax gross-ups to any of our executive officers. |

Forward-Looking Statements & Website References

This Proxy Statement contains “forward-looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995. Forward-looking statements may be identified by the use of words such as “anticipate,” “believe,” “expect,” “estimate,” “plan,” “outlook,” and “project” and other similar expressions that predict or indicate future events or trends or that are not statements of historical matters. Such forward-looking statements include, but are not limited to, statements regarding the Company’s plans, objectives, expectations, and intentions. Such statements are based on current expectations and are subject to numerous risks and uncertainties, many of which are outside of the control of Korn Ferry. Actual results may differ materially from those indicated by such forward-looking statements as a result of risks and uncertainties, including those factors discussed or referenced in our most recent annual report on Form 10-K filed with the SEC, under the heading “Risk Factors,” a copy of which is being made available with this Proxy Statement, and subsequent quarterly reports on Form 10-Q. Website references and hyperlinks throughout this document are provided for convenience only, and the content on the referenced websites is not incorporated by reference into this Proxy Statement, nor does it constitute a part of this Proxy Statement.

|

9

|

This page intentionally left blank

|

11

|

Election of Directors

Our stockholders will be asked to consider nine nominees for election to our Board to serve for a one-year term until the 2022 Annual Meeting of Stockholders and until their successors have been duly elected and qualified, subject to their earlier death, resignation, or removal. Each of the nominees was previously elected by stockholders at the 2020 Annual Meeting of Stockholders, except for Laura M. Bishop. Laura M. Bishop was identified as part of a thorough search process conducted by Korn Ferry’s internal board search consultants. As further described on page 30, in light of Ms. Gold’s and Mr. Shaheen’s continued and significant contributions as a director, the Board, at the recommendation of the Nominating and Corporate Governance Committee, exercised its right under the Corporate Governance Guidelines to nominate Ms. Gold and Mr. Shaheen to additional terms after their 74th birthdays.

The names of the nine nominees for director and their current positions, if any, with the Company are set forth in the table to the right. Detailed biographical information regarding each of these nominees is provided in this Proxy Statement under the heading “Background Information Regarding Director Nominees.” Our Nominating and Corporate Governance Committee has reviewed the qualifications of each of the nominees and has recommended to the Board that each nominee be submitted to a vote at the Annual Meeting.

All of the nominees have indicated their willingness to serve, if elected, but if any should be unable or unwilling to serve, proxies may be voted for a substitute nominee designated by the Board. Proxies cannot be voted for more than the number of nominees named in this Proxy Statement.

| Name | Position with Korn Ferry |

| Doyle N. Beneby | Director |

| Laura M. Bishop | Nominee |

| Gary D. Burnison | Director and Chief Executive Officer |

| Christina A. Gold | Director and Non-Executive Chair of the Board |

| Jerry P. Leamon | Director |

| Angel R. Martinez | Director |

| Debra J. Perry | Director |

| Lori J. Robinson | Director |

| George T. Shaheen | Director |

In uncontested elections, directors are elected by a majority of the votes cast, meaning that each director nominee must receive a greater number of shares voted “for” such nominee than the shares voted “against” such nominee. If an incumbent director does not receive a greater number of shares voted “for” such director than shares voted “against” such director, then such director must tender his or her resignation to the Board. In that situation, the Company’s Nominating and Corporate Governance Committee would make a recommendation to the Board about whether to accept or reject the resignation, or whether to take other action. Within 90 days from the date the election results were certified, the Board would act on the Nominating and Corporate Governance Committee’s recommendation and publicly disclose its decision and rationale behind it.

In a contested election, directors are elected by a plurality of the votes cast.

|

12

|

The Company’s Restated Certificate of Incorporation provides that the number of directors shall not be fewer than eight nor more than fifteen, with the exact number of directors within such limits to be determined by the Board. Currently, the Board is comprised of eight directors; following the election of directors at the Annual Meeting, the Board will be comprised of nine directors. Upon the recommendation of the Company’s Nominating and Corporate Governance Committee, the Board has nominated the following persons to serve as directors until the 2022 Annual Meeting of Stockholders or their earlier death, resignation or removal:

| Doyle N. Beneby | Angel R. Martinez |

| Laura M. Bishop | Debra J. Perry |

| Gary D. Burnison | Lori J. Robinson |

| Christina A. Gold | George T. Shaheen |

| Jerry P. Leamon |

Each of the named nominees is independent under the NYSE rules, except for Mr. Burnison. If reelected, Ms. Gold will continue to serve as the Company’s independent Non-Executive Chair of the Board.

The Board held 11 meetings during fiscal year 2021. Each of the incumbent directors attended at least 75% of the Board meetings and the meetings of committees of which they were members in fiscal year 2021. Directors are expected to attend each annual meeting of stockholders. The eight directors then-serving attended the 2021 Annual Meeting of Stockholders online.

Q & A with Doyle Beneby, Chair of the Nominating and Corporate Governance Committee

Question: In 2020, the Nominating and Corporate Governance Committee was given formal responsibility for overseeing the Company’s ESG Program. How has this informed the Nominating and Corporate Governance Committee’s activities, and what does the ESG Program encompass?

The Nominating and Corporate Governance Committee has continued to increase its oversight and involvement with the Company’s ESG Program, including overseeing the expansion of ESG disclosures and practices in the past year. Our ESG Program includes initiatives that seek to improve the way we work and live, empower Diversity, Equity, and Inclusion (“DE&I”), and give back to the communities in which we operate. The Proxy Statement Summary on page 3 highlights several recent ESG recognitions of which we are proud, and below are some of our ESG Program’s recent initiatives and accomplishments:

Reporting

| • | The Company published its third Corporate Responsibility Report, covering 2020 activities and achievements, and expanded ESG reporting to include an inaugural report in general alignment with the reporting recommendations for its industry by the Sustainability Accounting Standards Board. |

|

13

|

| • | Korn Ferry was awarded the 2021 Silver Status Medal from EcoVadis for its Corporate Social Responsibility (“CSR”) practices for the third consecutive year, and our score placed us in the top 16% of the more than 75,000 companies that EcoVadis assessed. |

| • | For the fourth consecutive year, Korn Ferry responded to the CDP Climate Change survey, reporting on our greenhouse gas emissions and broader practices related to climate change. Korn Ferry achieved a Management Level rating for our 2020 submission for having a strong awareness of our climate change impacts and opportunities, as well as managing them effectively. |

Human Capital Management and DE&I

| • | In fiscal year 2021, we launched the Mosaic Program, a global talent development program for an inclusive group of about 200 entry- and mid-level colleagues from across Korn Ferry’s business. The program includes one-on-one professional coaching, supervision, and sponsorship from the firm’s Global Operating Committee members, individual development plans, visible and complex project opportunities, and facilitated leadership development sessions. |

| • | Korn Ferry also offers a firm-wide mentorship program, empowering colleagues to learn, connect, and develop. We match mentors and mentees based on their proximity, career goals, and focus. The program is meant to reinforce our culture of collaboration, information-sharing, and personal development, allowing colleagues to discuss personal and professional growth and become more effective professionals. |

| • | Since 2018, Korn Ferry has maintained a Colleague Advisory Council that meets regularly to provide candid feedback directly to Mr. Burnison and other senior leaders on the colleague experience within Korn Ferry. Colleagues globally participate in the Council, which reflects Korn Ferry’s diverse geography, solutions, tenures/seniority, and other demographics and experiences. |

Philanthropy

| • | In 2020, we established an independent, not-for-profit: the Korn Ferry Charitable Foundation (the “Foundation”). The Foundation’s mission is to make real, lasting changes by helping people exceed their potential through opportunity. The Foundation’s first major initiative is Leadership U for Humanity, a leadership program developed by Korn Ferry for the Foundation with the goal of empowering professionals from underrepresented backgrounds. In seeking to make a significant impact, the Foundation is partnering with like-minded community organizations to help bring Leadership U for Humanity to a wide array of communities. With Korn Ferry’s support, Leadership U for Humanity is being made available at no cost to the program participants selected by the Foundation. |

Question: Inclusion is one of the Company’s four core values. As the Company continues to focus on DE&I and human capital management, how has the Board’s engagement on these topics changed over the past year?

The Board’s engagement regarding DE&I and human capital management matters has been an ongoing focus. As described above, Korn Ferry continues to invest in, develop, and champion internal programs and benefits intended to support global colleagues, and we discuss Korn Ferry’s current and potential workforce initiatives regularly with management. At the Board level, we are committed to active Board refreshment and to aligning Board composition and experience with the Company’s evolving needs. As part of the search process for each new director, the Nominating and Corporate Governance Committee seeks to include people from diverse backgrounds in the pool from which Board nominees are chosen. As a reflection of these efforts, our Board is currently more than 50% diverse and led by Board Chair Christina Gold, with 75% of Board leadership roles held by women or ethnically diverse directors. If elected at the Annual Meeting, Ms. Bishop will increase our Board’s diversity to include four women. We are proud of the Board’s diversity and representation.

|

14

|

The Board believes that the Board, as a whole, should possess a combination of skills, professional experience, and diversity of backgrounds necessary to oversee the Company’s business. In addition, the Board believes there are certain attributes every director should possess, as reflected in the Board’s membership criteria discussed below. Accordingly, the Board and the Nominating and Corporate Governance Committee consider the qualifications of directors and director candidates individually and in the broader context of the Board’s overall composition and the Company’s current and future needs.

The Nominating and Corporate Governance Committee is responsible for developing and recommending Board membership criteria to the full Board for approval. The criteria, which are set forth in the Company’s Corporate Governance Guidelines include:

| • | a reputation for integrity, |

| • | honesty and adherence to high ethical standards, |

| • | strong management experience, |

| • | current knowledge of and contacts in the Company’s industry or other industries relevant to the Company’s business, |

| • | the ability and willingness to commit adequate time and attention to Board and Committee activities, and |

| • | the fit of the individual’s skills and personality with those of other directors in building a Board that is effective, collegial, diverse, and responsive to the needs of the Company. |

The Nominating and Corporate Governance Committee seeks a variety of occupational, educational, and personal backgrounds on the Board in order to obtain a range of viewpoints and perspectives and to enhance the diversity of the Board in such areas as professional experience, geography, race, gender, and ethnicity. While the Nominating and Corporate Governance Committee does not have a formal policy with respect to diversity, the Nominating and Corporate Governance Committee believes it is essential that Board members represent diverse viewpoints and backgrounds. The Nominating and Corporate Governance Committee periodically evaluates the composition of the Board to assess the skills and experience that are currently represented on the Board, as well as the skills and experience that the Board will find valuable in the future, given the Company’s current business and strategic plans. This periodic assessment enables the Board to update the skills and experience it seeks in the Board as a whole and in individual directors as the Company’s needs evolve and change over time, and to assess the effectiveness of efforts to pursue diversity. In identifying director candidates from time to time, the Nominating and Corporate Governance Committee considers recommendations from Board members, management, and stockholders, and may from time to time engage a third-party search firm or utilize Company resources. The Nominating and Corporate Governance Committee may establish specific skills and experience that it believes the Company should seek in order to constitute a balanced and effective board.

In evaluating director candidates, and considering incumbent directors for renomination to the Board, the Nominating and Corporate Governance Committee takes into account a variety of factors. These include each nominee’s independence, financial literacy, personal and professional accomplishments, and experience, each in light of the composition of the Board as a whole and the needs of the Company in general, and for incumbent directors, past performance on the Board.

Reviewing Director Commitments. The Nominating and Corporate Governance Committee also considers each nominee’s or incumbent director’s ability and willingness to commit adequate time to Board and committee matters, including, for the Annual Meeting, Ms. Perry’s additional responsibilities as a board chair and member of three other public company or mutual fund complex boards, and in the case of Mr. Shaheen, his service on three other public company (and a wholly-owned subsidiary) board of directors.

Annual Board and Committee Evaluations

Each year, the Board and its committees conduct a self-evaluation to determine that it is functioning effectively and consistently with its purpose and responsibilities. Topics addressed through these processes have included Board structure, director nominations and recruitment, Board and committee meetings and information, Board responsibilities, including management succession planning, and Board and management relations.

| Solicit Feedback | Review By Outside Counsel | Internal Review | Discussion & Updates |

| Directors receive via secure website a detailed questionnaire designed to elicit feedback regarding the functioning and leadership of the Board and each of the committees as a whole. | Outside counsel reviews the responses to the questionnaire and consolidates the feedback into a summary presentation. | A summary of results are provided by outside counsel, with the anonymized responses, to the Chair of the Board and the Chair of the Nominating and Corporate Governance Committee for review. | The results are discussed at both the Board and Nominating and Corporate Governance Committee levels, along with a determination of what, if any, changes should be made in light of the responses. |

|

15

|

Board Composition: Skills, Tenure*, and Diversity

The Board and Company are focused on creating a Board that reflects a wide range of backgrounds, experiences, and cultures. The following skills are possessed by one or more of our nominees:

|

Extensive Senior Leadership / Executive Officer Experience (including as a public company Chief Executive Officer) |  |

Significant Public Company Board, Committee, and Corporate Governance Experience | |

|

Risk Management / Oversight Experience |  |

Innovative Thinking | |

|

Broad International Business Experience |  |

High Ethical Standards | |

|

Significant Finance, Tax, and Mergers and Acquisitions (“M&A”) Experience |  |

Appreciation of Diverse Cultures and Backgrounds | |

|

Accounting Expertise (including a Certified Public Accountant) |  |

Experience Overseeing Large and Diverse Workforces | |

|

Significant Strategic Oversight and Execution Experience |  |

Breadth of Experience Across Industries | |

|

Broad Product and Marketing Experience |  |

Information Security Expertise |

| * | Tenure is provided for non-executive directors only. |

| ** | These graphics include Mr. Shaheen’s cumulative service with the Board of Directors from 2009 to 2019, and from April 2020 to present. |

| *** | Not included in diversity percentages. |

|

16

|

Background Information Regarding Director Nominees

The biographies below set forth information about each of the director nominees, including each such person’s specific experience, qualifications, attributes, and skills that led our Board to conclude that such director nominee should serve on our Board in light of the Company’s current business, structure, and strategic plans. The process undertaken by the Nominating and Corporate Governance Committee in recommending qualified director candidates is described above under “Director Qualifications” and below under “Corporate Governance—Board Committees—Nominating and Corporate Governance Committee.”

|

Doyle N. BENEBY

Director Since: 2015

President and Chief Executive Officer, Midland Cogeneration Venture

Age: 61 |

Board Qualifications and Skills:

Extensive Senior Leadership/Executive Officer Experience: Currently serves as President and Chief Executive Officer of Midland Cogeneration Venture, and previously served in a multitude of senior leadership positions, including as former Chief Executive Officer of New Generation Power International, as President and Chief Executive Officer of CPS Energy, and various leadership roles at PECO Energy and Exelon Power, where he served as President.

Broad Energy Industry Experience: Over 30 years of experience in the energy industry, with expertise in many facets of the electric & gas utility industry.

Other Directorships:

Public Companies: Quanta Services and Capital Power Corporation

Other Companies: Midland Business Alliance |

Mr. Beneby has been the President and Chief Executive Officer of Midland Cogeneration Venture, a natural gas fired combined electrical energy and steam energy generating plant, since November 2018, and is also currently an independent consultant and professional director. Mr. Beneby previously served as Chief Executive Officer of New Generation Power International, a start-up international renewable energy company, based in Chicago, Illinois, from November 2015 until May 2016. Prior to that, Mr. Beneby served as President and Chief Executive Officer of CPS Energy, the largest municipal electric and gas utility in the nation, from July 2010 to November 2015. Prior to joining CPS Energy, Mr. Beneby served at Exelon Corporation from 2003 to 2010 in various roles, most recently, as President of Exelon Power and Senior Vice President of Exelon Generation from 2009 to 2010. From 2008 to 2009, Mr. Beneby served as Vice President, Generation Operations for Exelon Power. From 2005 to 2008, Mr. Beneby served as Vice President, Electric Operations for PECO Energy, a subsidiary of Exelon Corporation. Mr. Beneby also serves on the boards of Capital Power Corporation and Quanta Services, in addition to being a member of the board of the Midland Business Alliance.

|

17

|

|

Laura M. BISHOP

Nominee

Former Executive Vice President and Chief Financial Officer, USAA

Age: 59 |

Board Qualifications and Skills:

Senior Leadership/Executive Officer Experience: Held senior leadership positions over a nearly 20-year career with USAA, including as Executive Vice President and Chief Financial Officer, and in her near decade of work with Luby’s Inc., including as Senior Vice President and Chief Financial Officer.

Financial Experience and Investment Expertise: In addition to her service as Chief Financial Officer of both publicly traded and privately held companies, Ms. Bishop worked as a Senior Manager at Ernst & Young LLP early in her career and holds a Bachelor of Business Administration in Accounting.

Other Directorships:

Public Companies: N/A

Other Companies: N/A |

From 2001 to 2020, Ms. Bishop held a number of roles at USAA, a Fortune 100 integrated financial services company that provides financial products and services for the military and their families. Most recently, she served as the Executive Vice President and Chief Financial Officer of USAA from June 2014 until her retirement in December 2020, and in that role, served as the enterprise Chief Financial Officer for all of USAA’s operating companies spanning the Property and Casualty companies, USAA Federal Savings Bank, and USAA Life Insurance Company. As a member of USAA’s Executive Council, Ms. Bishop was also responsible for developing and executing strategy while directing activities across enterprise-wide financial management and reporting, including treasury, capital management, controller, tax, planning and forecasting, and strategic cost management. She was also responsible for governance and oversight for investment strategy and management of all institutional and benefit plan portfolios, as well as all capital markets activities, including commercial paper and long-term debt programs, credit facilities, asset-backed securitizations, and reinsurance programs. Prior to joining USAA in 2001, Ms. Bishop spent nine years with Luby’s Inc., a publicly traded restaurant company, where she served as Senior Vice President and Chief Financial Officer, among other leadership roles. Prior to that, Ms. Bishop served as a Senior Manager at Ernst & Young LLP, where she directed audits of publicly traded and privately held companies in a variety of industries.

|

Gary D. BURNISON

Director Since: 2007

President and Chief Executive Officer

Age: 60 |

Board Qualifications and Skills:

High Level of Financial Experience: Substantial financial experience gained in roles as President, Chief Executive Officer, and as former Chief Financial Officer and Chief Operating Officer of the Company, as Chief Financial Officer of Guidance Solutions, as an executive officer of Jefferies & Company, Inc., and as a partner at KPMG Peat Marwick.

Senior Leadership/Executive Officer Experience: In addition to serving as the Company’s President and Chief Executive Officer, served as Chief Financial Officer of Guidance Solutions.

Extensive Knowledge of the Company’s Business and Industry: Over 19 years of service with the Company, including as President and Chief Executive Officer of the Company since July 2007, Executive Vice President and Chief Financial Officer from March 2002 until June 2007, and Chief Operating Officer of the Company from October 2003 until June 2007.

Thought Leader: Author of seven leadership and career development books, and regular content focused on the intersection of strategy, talent, and leadership, as well as a frequent contributor to media outlets.

Other Directorships:

Public Companies: N/A

Other Companies: N/A |

Mr. Burnison has served as President and Chief Executive Officer of the Company since July 2007. He was the Executive Vice President and Chief Financial Officer of the Company from March 2002 until June 30, 2007. He also served as Chief Operating Officer of the Company from October 2003 until June 30, 2007. From 1999 to 2001, Mr. Burnison was Principal and Chief Financial Officer of Guidance Solutions and from 1995 to 1999 he served as an executive officer and member of the board of directors of Jefferies & Company, Inc., the principal operating subsidiary of Jefferies Group, Inc. Prior to that, Mr. Burnison was a partner at KPMG Peat Marwick.

|

18

|

|

Christina A. GOLD

Director Since: 2014

Chair of the Board

Age: 73 |

Board Qualifications and Skills:

Extensive Senior Leadership/Executive Officer Experience: Served in numerous senior leadership positions, including as Chief Executive Officer and President of The Western Union Company, President of Western Union Financial Services, Vice Chairman and Chief Executive Officer of Excel Communications, and President and CEO of Beaconsfield Group, Inc.

Broad International Experience: Significant international experience from 28-year career at Avon Products, Inc., including as Senior Vice President and President of Avon North America.

Significant Public Company Board Experience: Over 24 years of public company board experience, including as a director of International Flavors & Fragrances, Inc. since 2013, ITT Inc. (formerly ITT Corporation) from 1997 to 2020, Exelis Inc. from 2011 to 2013, and The Western Union Company from 2006 to 2010.

Other Directorships:

Public Companies: International Flavors & Fragrances, Inc.

Other Companies: Safe Water Network |

From September 2006 until her retirement in September 2010, Ms. Gold was Chief Executive Officer, President, and a director of The Western Union Company, a leading company in global money transfer. Ms. Gold was President of Western Union Financial Services, Inc. and Senior Executive Vice President of First Data Corporation, former parent company of The Western Union Company and provider of electronic commerce and payment solutions, from May 2002 to September 2006. Prior to that, Ms. Gold served as Vice Chairman and Chief Executive Officer of Excel Communications, Inc., a former telecommunications and e-commerce services provider, from October 1999 to May 2002. From 1998 to 1999, Ms. Gold served as President and Chief Executive Officer of Beaconsfield Group, Inc., a direct selling advisory firm that she founded. Prior to founding Beaconsfield Group, Ms. Gold spent 28 years (from 1970 to 1998) with Avon Products, Inc., in a variety of positions, including as Executive Vice President, Global Direct Selling Development, Senior Vice President, and President of Avon North America, and Senior Vice President and Chief Executive Officer of Avon Canada. Ms. Gold is currently a director of International Flavors & Fragrances, Inc. She also sits on the board of Safe Water Network, a non-profit organization working to develop locally owned, sustainable solutions to provide safe drinking water. From 1997 to 2020, Ms. Gold was a director of ITT Inc. (formerly ITT Corporation); from 2001 to 2020, she was a director of New York Life Insurance; and from October 2011 to May 2013, she was a director of Exelis, Inc. Ms. Gold also served a term on the Board of Governors of Carleton University in Ottawa Canada.

|

Jerry P. LEAMON

Director Since: 2012

Former Global Managing Director, Deloitte

Age: 70 |

Board Qualifications and Skills:

High Level of Financial Experience: Substantial financial experience gained from an almost 40-year career with Deloitte, including as leader of the tax practice and as leader of the M&A practice for more than 10 years.

Accounting Expertise: In addition to an almost 40-year career with Deloitte, Mr. Leamon is a certified public accountant.

Broad International Experience: Served as leader of Deloitte’s tax practice, both in the U.S. and globally, and was Global Managing Director for all client programs.

Service Industry Experience: Deep understanding of operational and leadership responsibilities within the professional services industry, having held senior leadership positions at Deloitte while serving some of their largest clients.

Other Directorships:

Public Companies: Credit Suisse USA, a subsidiary of Credit Suisse Group AG

Other Companies: Geller & Company, Americares Foundation, Jackson Hewitt Tax Services, and member of Business Advisory Council of the Carl H. Lindner School of Business |

Mr. Leamon served as Global Managing Director for Deloitte until his retirement in 2012, having responsibility for all of Deloitte’s businesses at a global level. In a career of almost 40 years at Deloitte, 31 of which as a partner, he held numerous roles of increasing responsibility. Previously, Mr. Leamon served as the leader of the tax practice, both in the U.S. and globally, and had responsibility as Global Managing Director for all client programs including industry programs, marketing communication and business development. In addition, Mr. Leamon was leader of the M&A practice for more than 10 years. Throughout his career, Mr. Leamon served some of Deloitte’s largest clients. Mr. Leamon serves on a number of boards of public, privately held, and non-profit organizations, including Credit Suisse USA, where he chairs the Audit Committee, Geller & Company, and Jackson Hewitt Tax Services, and he is Chairman of the Americares Foundation. Mr. Leamon is also a Limited Partner of Lead Edge Capital. He is also Trustee Emeritus of the University of Cincinnati Foundation and Board and serves as a member of the Business Advisory Council of the Carl H. Lindner School of Business. Mr. Leamon is a certified public accountant.

|

19

|

|

Angel R. MARTINEZ

Director Since: 2017

Former Chairman of the Board of Directors, and former Chief Executive Officer and President, of Deckers Brands

Age: 66 |

Board Qualifications and Skills:

Extensive Senior Leadership/Executive Officer Experience: Served in numerous senior leadership positions, including as Chief Executive Officer and President of Deckers Brands, Executive Vice President and Chief Marketing Officer of Reebok International Ltd., President of The Rockport Company, and President and Chief Executive Officer of Keen, LLC.

Broad Product and Marketing Experience: Almost 40 years of experience in product and marketing from senior positions with, among other companies, Deckers Brands, Reebok International, and The Rockport Company.

Significant Public Company Board and Corporate Governance Experience: Over 22 years of public company board service, including as a director of Tupperware Brands Corporation from 1998 to 2020 and Chairman of the Board of Deckers Brands from 2008 to 2017.

Other Directorships:

Public Companies: Genesco Inc.

Other Companies: N/A |

Mr. Martinez is the former President, Chief Executive Officer, and Chairman of the Board of Directors of Deckers Brands (formerly known as Deckers Outdoor Corporation) (“Deckers”). Deckers is a global leader in designing, marketing, and distributing innovative footwear, apparel, and accessories developed for both everyday casual lifestyle use and high performance activities. He served as Chief Executive Officer and President of Deckers from April 2005 until his retirement in June 2016, as Executive Chairman of the Board from 2008 until June 2016, and as non-executive Chairman from June 2016 until September 2017. Prior to joining Deckers, he was President, Chief Executive Officer, and Vice Chairman of Keen LLC, an outdoor footwear manufacturer, from April 2003 to March 2005. Prior thereto, he served as Executive Vice President and Chief Marketing Officer of Reebok International Ltd. (“Reebok”) and as Chief Executive Officer and President of The Rockport Company, a subsidiary of Reebok. He has served as a member of the board of Genesco Inc. since May 2021. Mr. Martinez graduated from the University of California, Davis, in 1977.

|

20

|

|

Debra J. PERRY

Director Since: 2008

Former senior managing director in the Global Ratings and Research Unit of Moody’s Investors Service, Inc.

Age: 70 |

Board Qualifications and Skills:

High Level of Financial Experience: Substantial financial experience gained from 23 years of professional experience in financial services, including a 12-year career at Moody’s Corporation, where among other things, Ms. Perry oversaw the Americas Corporate Finance, Leverage Finance, and Public Finance departments.

Significant Audit Committee Experience: Over 16 years of public company audit committee service, including as a member of MBIA Inc.’s Audit Committee (2004 to 2008), PartnerRe’s Audit Committee (from June 2013 to March 2016, including as Chair of the Audit Committee from January 2015 to March 2016), Korn Ferry’s Audit Committee (since 2008; appointed Chair of Audit Committee in 2010), and The Bernstein Funds, Inc.’s Audit Committee (since 2011).

Significant Public Company Board and Corporate Governance Experience: Previously served as a director (June 2013 to March 2016) and Chair of the Audit Committee (January 2015 to March 2016) of PartnerRe, and as a director of BofA Funds Series Trust (June 2011 to April 2016), MBIA Inc. (2004 to 2008), and CNO Financial Group, Inc. (2004 to 2011). Actively involved in corporate governance organizations, including the National Association of Corporate Directors (“NACD”). Named in 2014 to NACD’s Directorship 100, which recognizes the most influential people in the boardroom and corporate governance community.

Other Directorships:

Public Companies: Assurant and Genworth Financial Inc.

Other Companies: The Bernstein Funds, Inc., a mutual fund complex |

Ms. Perry currently serves on the boards of directors of Assurant (as well as its Finance & Risk Committee, which she chairs, and its Nominating and Governance Committee) (elected August 2017), Genworth Financial Inc. (as well as its Audit Committee and Risk Committee, which she chairs) (elected December 2016), and The Bernstein Funds, Inc. (a mutual fund complex that includes the Sanford C. Bernstein Fund, Inc., Bernstein Fund and A/B Multi-Manager Alternative Fund) (elected July 2011 and Chair since July 2018, as well as its Audit Committee and Nominating Committee). She was a member of the Board (from June 2013) and Chair of the Audit Committee (from January 2015) of PartnerRe, a Bermuda-based reinsurance company, until the sale of the company to a European investment holding company in March 2016. She was also a trustee of the Bank of America Funds from June 2011 until April 2016, where she served as Chair of the Board’s Governance Committee. Ms. Perry served on the Board of Directors and Chair of the Human Resources and Compensation Committee of CNO Financial Group, Inc. from 2004 to 2011.

In 2014, Ms. Perry was named to NACD’s Directorship 100, which recognizes the most influential people in the boardroom and corporate governance community. From September 2012 to December 2014, Ms. Perry served as a trustee of the Executive Committee of the Committee for Economic Development (“CED”) in Washington, D.C., a non-partisan, business-led public policy organization, until its merger with the Conference Board, and she continues as a trustee of CED. She worked at Moody’s Corporation from 1992 to 2004, when she retired. From 2001 to 2004, Ms. Perry was a senior managing director in the Global Ratings and Research Unit of Moody’s Investors Service, Inc. where she oversaw the Americas Corporate Finance, Leverage Finance, Public Finance, and Financial Institutions departments. From 1999 to 2001, Ms. Perry served as Chief Administrative Officer and Chief Credit Officer, and from 1996 to 1999, she was a group managing director for the Finance, Securities, and Insurance Rating Groups, of Moody’s Corporation.

|

21

|

|

Lori J. ROBINSON

General (ret.)

Director Since: 2019

Commander, U.S. Northern Command and North American Aerospace Defense Command, Department of the Air Force (Ret.)

Age: 62 |

Board Qualifications and Skills:

High Level of Leadership Experience: Four Star General and first female U.S. Combatant Commander, with numerous government leadership roles with the U.S. Department of Defense, including serving as Commander of the U.S. Northern Command and North American Aerospace Defense Command, and Commander, Pacific Air Forces and Air Component Commander for U.S. Pacific Command, leading more than 45,000 Airmen.

Significant Strategic Oversight and Execution Experience: Over three decades of experience with the U.S. Air Force overseeing, among other things, homeland defense, civil support, and security cooperation.

Extensive International Experience: Interacted with counterparts in the Indo-Pacific (including China) and the Middle East, reported directly to the U.S. Secretary of Defense and Chief of the Canadian Defence Staff, served four combat tours, and oversaw U.S. Air Force operations in the Middle East.

Other Directorships:

Public Companies: Nacco Industries and Centene Corp.

Other Companies: The Robinson Group, LLC |

Gen. (ret.) Robinson brings to the Board over three decades of experience with the U.S. Air Force, having most recently served as the Commander of the U.S. Northern Command (“USNORTHCOM”) and North American Aerospace Defense Command (“NORAD”) of the Department of Defense from 2016 to 2018, when she retired. USNORTHCOM partners to connect homeland defense, civil support, and security cooperation to defend and secure the United States and its interests, while NORAD conducts aerospace warning, aerospace control, and maritime warning in the defense of North America. Gen. (ret.) Robinson previously served as Commander, Pacific Air Forces and Air Component Commander for U.S. Pacific Command, from 2014 to 2016, and as Vice Commander, Air Combat Command, from 2013 to 2014. The Pacific Air Forces delivers space, air, and cyberspace capabilities to support the U.S. Indo-Pacific Command’s objectives, and the U.S. Pacific Command is responsible for defending and promoting U.S. interests in the Pacific and Asia. Gen. (ret.) Robinson has also commanded an air control wing, an operations group, and a training wing; served as Director of the Secretary of the Air Force and Chief of Staff of the Air Force Executive Action Group at the Pentagon; and Director, Legislative Liaison, Office of the Secretary of the Air Force with the Pentagon, among a number of other leadership positions. Gen. (ret.) Robinson is a Four Star General and was the first female Combatant Commander for the United States. She was also an Air Force Fellow at The Brookings Institution in Washington, D.C. in 2002. Since retiring, Gen. (ret.) Robinson joined the Harvard Kennedy School, Belfer Center for Science and International Affairs in 2018, as a non-resident Senior Fellow where she shares her insights on leadership, public service, and international security issues with faculty, staff, and students. Gen. (ret.) Robinson is also an active speaker, which she pursues through The Robinson Group, LLC, an organization she founded for such purposes and of which she is also a director. Gen. (ret.) Robinson has been a member of the board of directors of Nacco Industries since September 2019, and of Centene Corp. since October 2019.

|

George T. SHAHEEN

Director Since: 2020

(previously a director from 2009 to 2019)

Former Chief Executive Officer of Siebel Systems, Inc.

Age: 77 |

Board Qualifications and Skills:

Extensive Senior Leadership/Executive Officer Experience: Previously served as Chief Executive Officer of Siebel Systems, Inc., Chief Executive Officer and Global Managing Partner of Andersen Consulting, and CEO of Webvan Group, Inc.

Significant Public Company Board Experience: 16 years of public company board experience, including as a director of NetApp (since 2004), Marcus & Millichap (since 2013), and Green Dot Corporation (since 2013).

Service Industry Experience: Former Chief Executive Officer of Andersen Consulting.

Other Directorships:

Public Companies: NetApp, Marcus & Millichap, and Green Dot Corporation and its wholly owned subsidiary, Green Dot Bank

Other Companies: [24]7.ai |

Mr. Shaheen, who served as non-executive Chair of our Board from 2012 to 2019, was Chief Executive Officer of Siebel Systems, Inc., a CRM software company, which was purchased by Oracle in January 2006, from April 2005 to January 2006, when he retired. He was Chief Executive Officer and Global Managing Partner of Andersen Consulting, which later became Accenture, from 1989 to 1999. He then became Chief Executive Officer and Chairman of the Board of Webvan Group, Inc. from 1999 to 2001. Mr. Shaheen serves on the boards of NetApp, [24]7.ai, Marcus & Millichap, and Green Dot Corporation (including its wholly owned subsidiary, Green Dot Bank). He also served on the Strategic Advisory Board of Genstar Capital. He has served as IT Governor of the World Economic Forum, and was a member of the Board of Advisors for the Northwestern University Kellogg Graduate School of Management. He has also served on the Board of Trustees of Bradley University. Mr. Shaheen received a BS degree and an MBA from Bradley University.

|

22

|

The Board oversees the business and affairs of the Company and believes good corporate governance is a critical factor in our continued success and also aligns management and stockholder interests. Through our website, at www.kornferry.com, our stockholders have access to key governing documents such as our Code of Business Conduct and Ethics, Corporate Governance Guidelines, and charters of each committee of the Board, as well as information regarding our Corporate Responsibility Program. The highlights of our corporate governance program are included below:

|

|

|

||

| Board Structure | Stockholder Rights | Other Highlights | ||

|

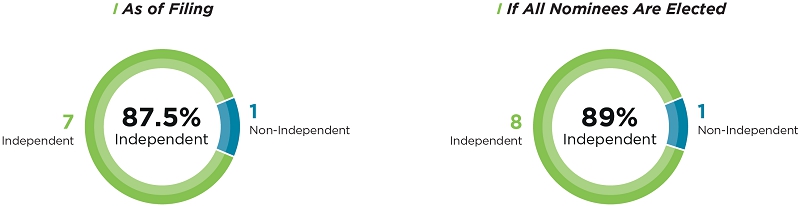

• 87.5% of the Board consists of Independent Directors • Independent Chair of the Board, Separate from CEO • Independent Audit, Compensation, and Nominating Committees • Regular Executive Sessions of Independent Directors • Annual Board and Committee Self- Evaluations • 67% Diverse Board Members and nominees (if all are elected) • Female Chair of the Board and 2 Committees Led by Diverse Directors (by Gender or Race/ Ethnicity) • Annual Strategic Off-Site Meeting • No Director Serves on More than Four Public Company Boards • 10-Term Service Limit for Non-Executive Directors Joining the Board after October 1, 2020 |

• Annual Election of All Directors • Majority Voting for Directors in Uncontested Elections • No Poison Pill in Effect • Stockholder Communication Process for Communicating with the Board • Regular Stockholder Engagement • No Supermajority Voting Standards • Ability of Stockholders to Call Special Stockholder Meetings |

• Clawback Policy • Stock Ownership Policy • Pay-for-Performance Philosophy • Policies Prohibiting Hedging, Pledging, and Short Sales • No Excise Tax Gross-Ups • Quarterly Education on Latest Corporate Governance Developments • Committee Oversight of ESG Program • Board Oversight of Political Contributions and Risk |

The Company’s Corporate Governance Guidelines provide that the Board is free to select its Chair and Chief Executive Officer in the manner it considers to be in the best interests of the Company and that the role of Chair and Chief Executive Officer may be filled by a single individual or two different persons. This provides the Board with flexibility to decide what leadership structure is in the best interests of the Company at any point in time. Currently, the Board is led by an independent, non-executive Chair, Ms. Gold. Ms. Gold will continue to serve as Chair of the Board, subject to her reelection as a director at the Annual Meeting. The Board has determined that having an independent director serve as Chair of the Board is in the best interests of the Company at this time as it allows the Chair to focus on the effectiveness and independence of the Board while the Chief Executive Officer focuses on executing the Company’s strategy and managing the Company’s business. In the future, the Board may determine that it is in the best interests of the Company to combine the role of Chair and Chief Executive Officer.

| 23 | |

| 2021 Proxy Statement | 2021 Proxy Statement |

The Board has determined that as of the date hereof a majority of the Board is “independent” under the independence standards of The New York Stock Exchange (the “NYSE”). The Board has determined that the following directors and nominees are “independent” under the independence standards of the NYSE: Doyle N. Beneby, Laura M. Bishop, Christina A. Gold, Jerry P. Leamon, Angel R. Martinez, Debra J. Perry, Lori J. Robinson, and George T. Shaheen.

For a director to be “independent,” the Board must affirmatively determine that such director does not have any material relationship with the Company. To assist the Board in its determination, the Board reviews director independence in light of the categorical standards set forth in the NYSE’s Listed Company Manual. Under these standards, a director cannot be deemed “independent” if, among other things:

| • | the director is, or has been within the last three years, an employee of the Company, or an immediate family member is, or has been within the last three years, an executive officer of the Company; |

| • | the director has received, or has an immediate family member who received, during any 12-month period within the last three years, more than $120,000 in direct compensation from the Company, other than director and committee fees and pension or other forms of deferred compensation for prior service (provided such compensation is not contingent in any way on continued service); |

| • | (1) the director or an immediate family member is a current partner of a firm that is the Company’s internal or external auditor, (2) the director is a current employee of such a firm, (3) the director has an immediate family member who is a current employee of such a firm and personally works on the Company’s audit, or (4) the director or an immediate family member was within the last three years a partner or employee of such firm and personally worked on the Company’s audit within that time; |

| • | the director or an immediate family member is, or has been within the last three years, employed as an executive officer of another company where any of the Company’s present executive officers at the same time serve or served on that company’s compensation committee; or |

| • | the director is a current employee, or an immediate family member is a current executive officer, of a company that has made payments to, or received payments from, the Company for property or services in an amount which, in any of the last three fiscal years, exceeds the greater of $1 million or 2% of the other company’s consolidated gross revenues. |

The independent directors of the Board meet regularly in executive sessions outside the presence of management. Ms. Christina Gold, as Chair of the Board, currently presides at all executive sessions of the independent directors.

| 24 | |

| | 2021 Proxy Statement |

Board’s Oversight of Enterprise Risk and Risk Management

The Board plays an active role, both as a whole and also at the committee level, in overseeing the Company’s management of risks. Management is responsible for the Company’s day-to-day risk management activities. The Company has established an enterprise risk framework for identifying, aggregating, and evaluating risk across the enterprise. The risk framework is integrated with the Company’s annual planning, audit scoping, and control evaluation management by its internal auditor. The review of risk management is a dedicated periodic agenda item for the Audit Committee, and the Company’s other Board committees also consider and address risk during the course of their performance of their committee responsibilities, as summarized in the following graphic.

| The Board | ||

| Oversees Company process for assessing and managing risk | ||

| Monitors risks through regular reports from each committee chair and the General Counsel | ||

| Apprised of particular risk management matters in connection with its general oversight and approval of corporate matters, including, but not limited to, cyber security | ||

|

|

|

|

||||

| Audit Committee |

Nominating and Corporate Governance Committee |

Compensation and Personnel Committee |